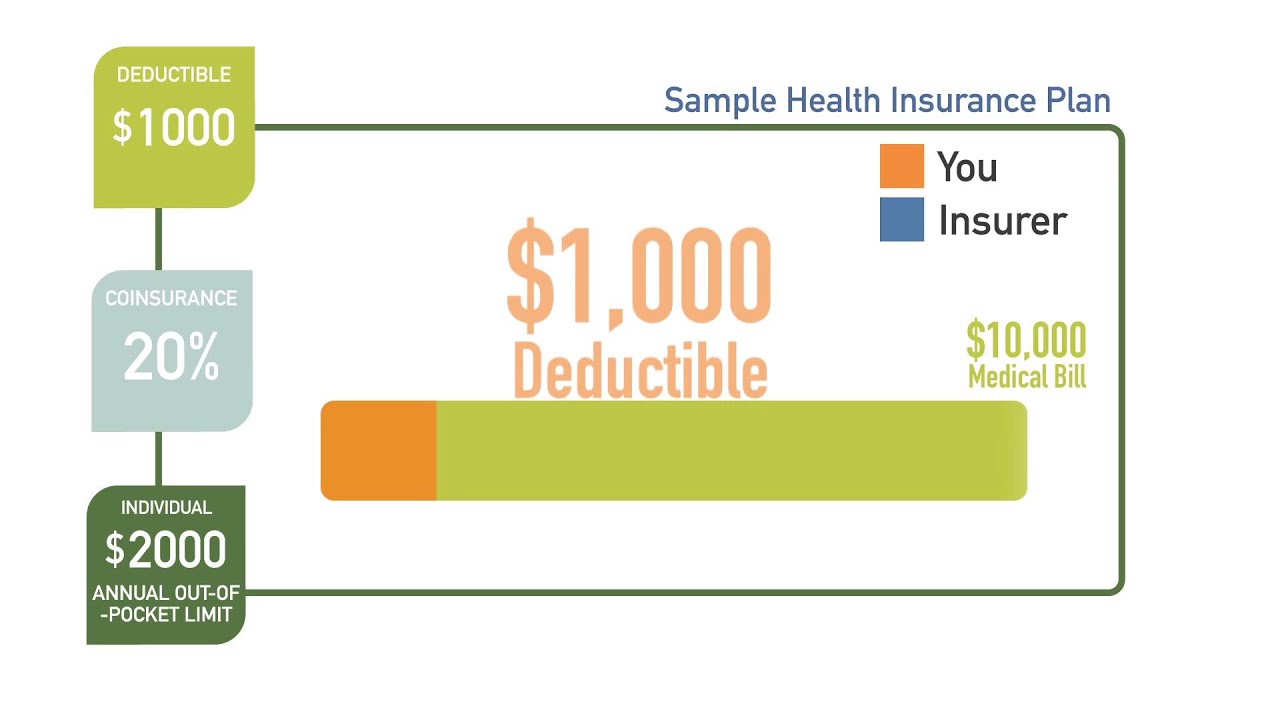

It likewise can offer you with info to figure out if the plan is thought about budget-friendly to you (Institutions are required by the u.s. Public health service to do which of the following:). When using the Health Insurance Marketplace Calculator, you can respond to "No" to Question # 4 if your company's protection is unaffordable or does not fulfill the minimum value requirement. While medical insurance may pay for the majority of a covered medical service, you typically still pay a few of the expense when you go to the doctor or have a hospital stay. Actuarial value is the percentage of total covered medical expenses that are paid for by the insurance company, usually, for a normal population.

For instance, if a plan has an actuarial value of 70%, then the insurer will pay about 70% of the overall medical costs for everybody covered by that plan. Together, you and everybody enrolled in the strategy would pay the staying 30% of the overall costs. This does not imply that you personally will pay 30% of your expenditures. Rather, this is a typical throughout everyone enrolled in the plan. Your own costs will differ significantly from this quantity, depending upon just how much care you utilize. While actuarial worth does not tell you precisely what you will pay, understanding it can assist you select which level of strategy is best for your health requirements.

Bronze strategies will have low monthly premiums, however if you get ill or have an accident you will pay more in medical bills. Silver plans are rather more financially protective and have an actuarial value of about 70%. Gold and Platinum plans have the highest monthly payments but also are the most protective if you get sick or require a lot of medical care: they have actuarial worths of about 80% and 90%, respectively. Once you select which level of protection is ideal for you, you can compare plans of a similar value side-by-side. If your income is really restricted, you may receive a cost-sharing subsidy if you sign up for a silver plan (these subsidies are explained more above).

Normally silver plans have an actuarial value of 70%, but with the cost-sharing aid, your silver plans' actuarial value will vary from 73% to 94% (depending on your income). This implies you will likely pay less when you go to the physician or health center than you otherwise would with a silver more info plan. The Medical Insurance Marketplace Calculator estimates whether you may be qualified for cost staring subsidies. If you are likely eligible for a cost sharing aid, the calculator also shows what your silver plan's actuarial value would be.

March 20, 2014 Picking a health insurance can be made complex. We can help you comprehend how to compare Market strategies and pick one that's right for you. Here are some crucial things to think about when choosing a strategy: There are 5 categories of Market insurance strategies: Bronze, Silver, Gold, Platinum, and Catastrophic. The health insurance category you pick determines how you and your plan share the expenses of care. This is the quantity you pay your insurer for your strategy whether you use medical services or not. Month-to-month premiums are very important, however they're not all you need to consider.

You pay these out-of-pocket costs in addition to your monthly premiums. Various strategy types offer different levels of coverage for care you get inside and outside of the strategy's network of medical professionals, hospitals, drug stores, and other medical provider. All plans offered through the Market supply the same vital health benefits, cover pre-existing conditions and provide complimentary preventive services. Now that you understand what to search for you can sneak peek strategies and costs in your area and apply online. It takes most individuals 20 minutes or less to use.

Lots of or all of the products featured here are from our partners who compensate us. This might affect which items we blog about and where and how the product appears on a page. However, this does not affect our evaluations. Our viewpoints are our own. Time is usually limited to choose the very best medical insurance plan for your family, but hurrying and choosing the incorrect one can be expensive. Here's a start-to-finish guide to choosing the very best prepare for you and your family, whether it's through the federal market or a company. The majority of people with medical insurance get it through an employer.

The Ultimate Guide To Who World Health Organization

Basically, your business is your marketplace. If your company provides medical insurance and you want to search for an alternative strategy in the exchanges, you can. However strategies in the market are most likely to cost check here a lot more. This is due to the fact that a lot of employers pay a portion of employees' insurance coverage premiums and since the strategies have lower overall premiums, usually. If your job does not provide health insurance coverage, store on your state's public market, if offered, or the federal market to discover the most affordable premiums. Start by going to Health, Care. gov and entering your ZIP code throughout open enrollment. You'll be sent out to your state's exchange if there is one.

You can likewise buy medical insurance through a personal exchange or directly from an insurer. If you select these choices, you will not be eligible for superior tax credits, which are income-based discounts on your month-to-month premiums. You'll experience some alphabet soup while shopping; the most typical kinds of medical insurance policies are HMOs, PPOs, EPOs or POS plans. The kind you choose will assist identify your out-of-pocket costs and which physicians you can see. While comparing plans, search for a summary of benefits. Online marketplaces generally supply a link to the summary and show the expense near the strategy's title.

If you're going through an employer, ask your work environment advantages administrator for the summary of advantages. When comparing different strategies, put your family's medical requirements under the microscope. Take a look at the quantity and kind of treatment you've received in the past. Though it's impossible to forecast every Mental Health Delray medical cost, understanding patterns can assist you make a notified choice. If you choose an HMO or POS plan, which need recommendations, you normally should see a medical care doctor prior to arranging a treatment or visiting a specialist. Because of this requirement, many individuals prefer other plans. Due to the constraints, however, HMOs tend to be the most affordable kind of health insurance, overall.

One benefit is that there's less work on your end, since your doctor's personnel coordinates check outs and deals with medical records. If you do select a POS plan and go out of network, ensure to get the referral from your physician ahead of time to lower out-of-pocket expenses. If you would rather choose your professionals, you might be happier with a PPO or an EPO. An EPO might assist keep costs low as long as you find suppliers in network; this is more likely to be the case in a bigger city location. A PPO may be better if you live in a remote or rural area with restricted access to medical professionals and care, as you might be required to go out of the network.